40-42 Hatton

Garden London

EC1N 8EB

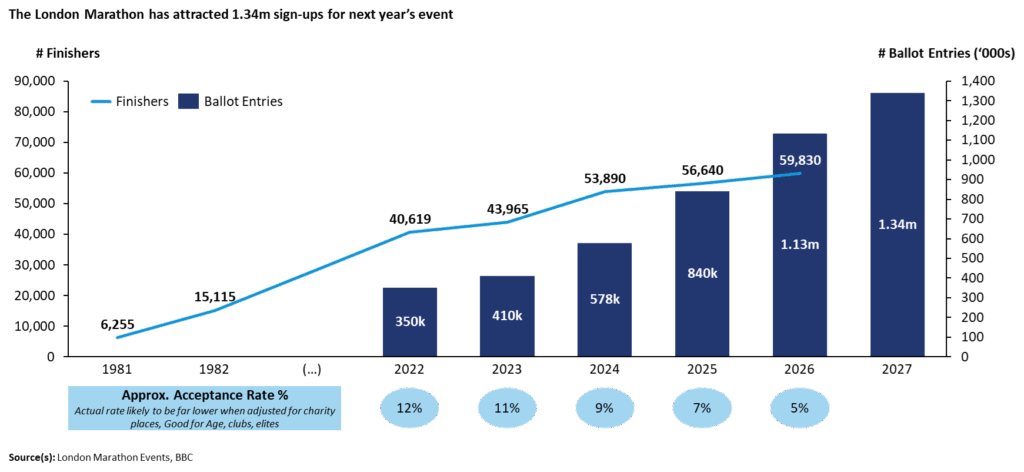

On Sunday 29 March 1981, 6,255 individuals crossed the finish line of the inaugural London Marathon. 45 years later, at the race’s 2026 edition, that figure exceeded 59,000. This may seem a large figure – and indeed, it was a new world record for number of finishers at a marathon – but it was still only a fraction of the 1.13m people who signed up. For next year’s event, the number of ballot entries stands at 1.34m.

The logical conclusion is that demand is far outstripping supply. Implied ballot acceptance rates have declined to 5% as of 2026. When adjusted for non-ballot routes (e.g. charity places, Good For Age, club spots, championship places), the rate may be as low as 2-3%.

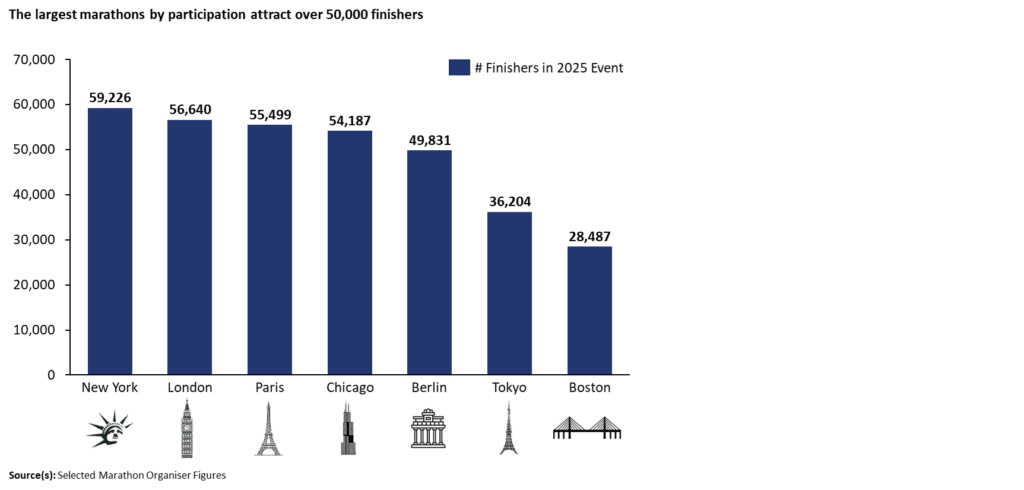

London is not an anomaly in the scale of its marathon. In 2025, New York saw 59,226 finishers – a new world-record until bested by London 2026. Paris, Chicago, and Berlin all reported numbers in the same ballpark. The world’s largest marathons converge around the 50-60k mark not because of appetite, but because of inherent supply-side constraints that all events of this nature must grapple with, such as permits, road closures, and volunteer hours.

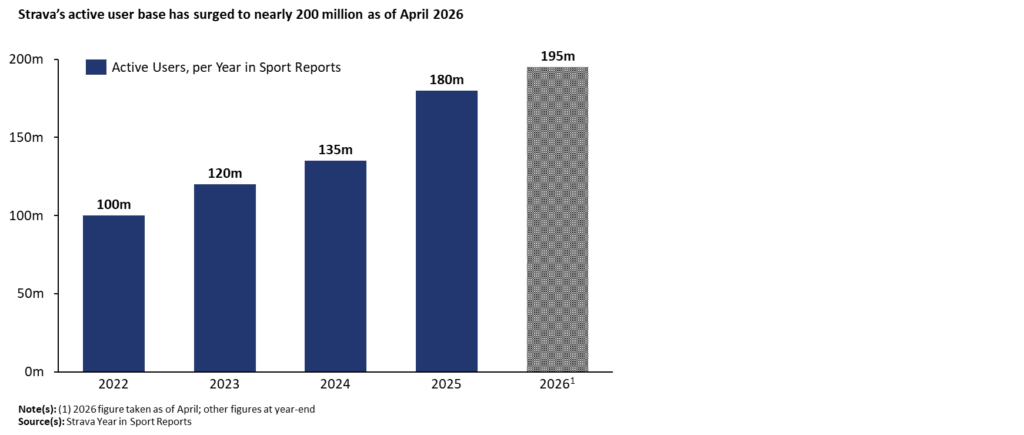

While London’s extraordinary ballot numbers are no doubt partly driven by the infectious community support and the universal recognition of the feat, they also provide reasonable evidence of the sheer demand for running. So too does the continued growth in Strava’s active user base. Whether or not they get a coveted London spot, for the vast number of those actively and passively interested in running, where does their time (and spend) go?

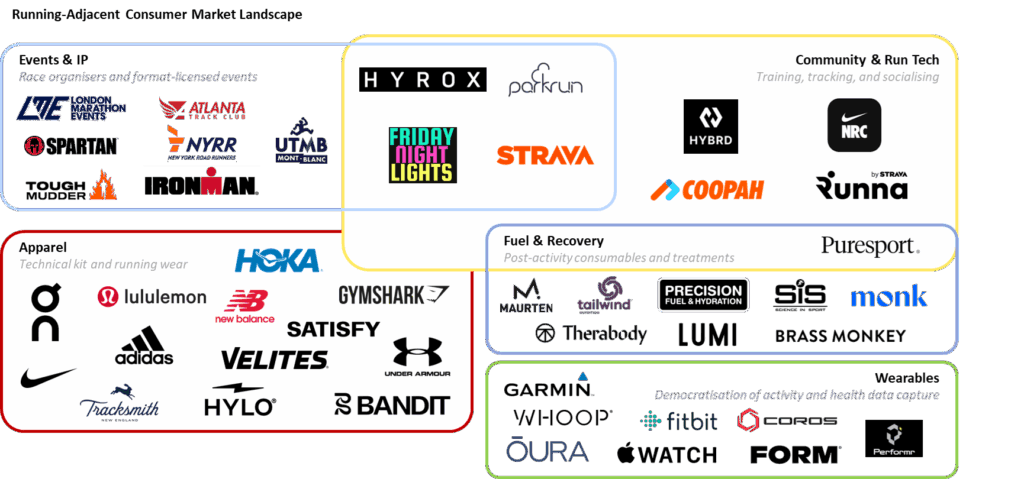

We can segment the running-adjacent market into five categories: Events & IP, Community & Run Tech, Apparel, Fuel & Recovery, and Wearables.

Hyrox, parkrun, Friday Night Lights, and Strava all sit in the intersection of the first two areas. Each is simultaneously something to train with/for and something to belong to. Strava has long been the leader in providing the underlying consumer tech that sits below the rest of what people do in the running market. For the others, they each entered the market as an event, but retained their users off the back of community.

Hyrox offers the clearest illustration. From 650 participants at its inaugural event in Hamburg in 2017, it is expected to attract up to 1.5m athletes across the 25/26 season, supported by thousands of affiliated gyms globally. The major competitive advantage over traditional events is the lack of supply-side constraints. Where major marathons are capping out at ~60k participants, Hyrox can scale far past this by simply expanding horizontally across gyms. Start-ups in this space will note Hyrox as a new market leader, but white space remains for niche format-licensed events with a clearly unique positioning.

Perhaps the clearest underserved gap on the chart is the AI-native training and coaching space. Running coach Coopah, hybrid-training app Hybrd, and the now Strava-owned Runna are among the most visible names. Software margins, recurring revenue, and a rapidly expanding addressable market make this a natural fit for venture capital. Strava’s 2025 acquisitions of Runna and The Breakaway suggest the dominant exit path is likely to be acquisition by a platform underneath the category.

Apparel has attracted the most public-market attention. On Holding reported 2025 revenue of CHF 3.0bn, up 30% at a 63% gross margin, closer to luxury goods than athletic apparel. The rising star Hoka generated $2.2bn in FY25, up 24%. Other market giants Nike, Adidas, and Lululemon make up most of the rest of the premium tier. More contested is the tier below, in brands like Tracksmith, Satisfy, and Bandit, where identity is the driving force behind purchase decisions. However, inventory and working capital requirements make apparel a more challenging venture play.

Wearables are largely consolidated by household names and largely closed to new entrants, though start-ups with a valid differentiator may be successful in capturing share. Fuel and recovery is populated by founder-led D2C brands; the consumables side is mature, led by players like Maurten, Precision, and SiS, while the recovery sub-segment is younger and more fragmented.

There can be no question that the running boom is upon us. Where we can be less certain is which structures around this boom are durable, and where capacity still exists for new entrants. London Marathon ballot entries will keep growing faster than the finisher base; the overflow has to go somewhere.

https://www.bbc.co.uk/sport/athletics/articles/cd6p081y698o

![]()

Ready to take your sports start-up to the next level? Let's collaborate and redefine the game together.

On Sunday 29 March 1981, 6,255 individuals crossed the finish line of the inaugural London Marathon. 45 years later, at the race’s 2026 edition, that figure exceeded 59,000. This may seem a large figure – and indeed, it was a new world record for number of finishers at a marathon – but it was still only a fraction of the 1.13m people who signed up. For next year’s event, the number of ballot entries stands at 1.34m.

The logical conclusion is that demand is far outstripping supply. Implied ballot acceptance rates have declined to 5% as of 2026. When adjusted for non-ballot routes (e.g. charity places, Good For Age, club spots, championship places), the rate may be as low as 2-3%.

London is not an anomaly in the scale of its marathon. In 2025, New York saw 59,226 finishers – a new world-record until bested by London 2026. Paris, Chicago, and Berlin all reported numbers in the same ballpark. The world’s largest marathons converge around the 50-60k mark not because of appetite, but because of inherent supply-side constraints that all events of this nature must grapple with, such as permits, road closures, and volunteer hours.

While London’s extraordinary ballot numbers are no doubt partly driven by the infectious community support and the universal recognition of the feat, they also provide reasonable evidence of the sheer demand for running. So too does the continued growth in Strava’s active user base. Whether or not they get a coveted London spot, for the vast number of those actively and passively interested in running, where does their time (and spend) go?

We can segment the running-adjacent market into five categories: Events & IP, Community & Run Tech, Apparel, Fuel & Recovery, and Wearables.

Hyrox, parkrun, Friday Night Lights, and Strava all sit in the intersection of the first two areas. Each is simultaneously something to train with/for and something to belong to. Strava has long been the leader in providing the underlying consumer tech that sits below the rest of what people do in the running market. For the others, they each entered the market as an event, but retained their users off the back of community.

Hyrox offers the clearest illustration. From 650 participants at its inaugural event in Hamburg in 2017, it is expected to attract up to 1.5m athletes across the 25/26 season, supported by thousands of affiliated gyms globally. The major competitive advantage over traditional events is the lack of supply-side constraints. Where major marathons are capping out at ~60k participants, Hyrox can scale far past this by simply expanding horizontally across gyms. Start-ups in this space will note Hyrox as a new market leader, but white space remains for niche format-licensed events with a clearly unique positioning.

Perhaps the clearest underserved gap on the chart is the AI-native training and coaching space. Running coach Coopah, hybrid-training app Hybrd, and the now Strava-owned Runna are among the most visible names. Software margins, recurring revenue, and a rapidly expanding addressable market make this a natural fit for venture capital. Strava’s 2025 acquisitions of Runna and The Breakaway suggest the dominant exit path is likely to be acquisition by a platform underneath the category.

Apparel has attracted the most public-market attention. On Holding reported 2025 revenue of CHF 3.0bn, up 30% at a 63% gross margin, closer to luxury goods than athletic apparel. The rising star Hoka generated $2.2bn in FY25, up 24%. Other market giants Nike, Adidas, and Lululemon make up most of the rest of the premium tier. More contested is the tier below, in brands like Tracksmith, Satisfy, and Bandit, where identity is the driving force behind purchase decisions. However, inventory and working capital requirements make apparel a more challenging venture play.

Wearables are largely consolidated by household names and largely closed to new entrants, though start-ups with a valid differentiator may be successful in capturing share. Fuel and recovery is populated by founder-led D2C brands; the consumables side is mature, led by players like Maurten, Precision, and SiS, while the recovery sub-segment is younger and more fragmented.

There can be no question that the running boom is upon us. Where we can be less certain is which structures around this boom are durable, and where capacity still exists for new entrants. London Marathon ballot entries will keep growing faster than the finisher base; the overflow has to go somewhere.

https://www.bbc.co.uk/sport/athletics/articles/cd6p081y698o

Accelerate Ventures 40-42 Hatton Garden London EC1N 8EB