40-42 Hatton

Garden London

EC1N 8EB

What started as a $20,000 esports tournament in South Korea in 2000 has evolved into a global phenomenon, with the Esports World Cup in Riyadh now offering a staggering $60 million prize pool.

Over the past 24 years, esports has undergone explosive growth, driven by key milestones such as the rise of Twitch and the surge in streamers and viewers as a result of the Covid-19 pandemic. In just the last five years, esports revenue has more than tripled, reaching $3.8 billion in 2023. As a rapidly expanding industry, esports remains full of untapped revenue, presenting exciting opportunities in the years ahead.

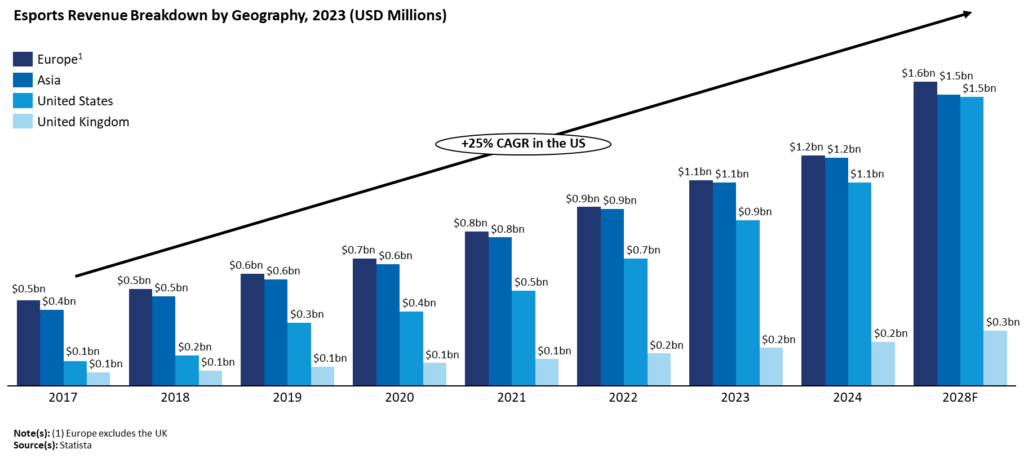

Europe leads as the largest market

While Europe remains the largest market for esports globally, both now and in the foreseeable future, the US market is expanding at a much faster pace – growing three times quicker on average than Asia, Europe, and the UK. With a substantial population of gamers and esports enthusiasts, the US has seen esports rapidly gain traction as both entertainment and competitive sport. Notably, several US universities now offer esports scholarships and programs, further legitimising esports as a viable career path and attracting a new generation of players and fans.

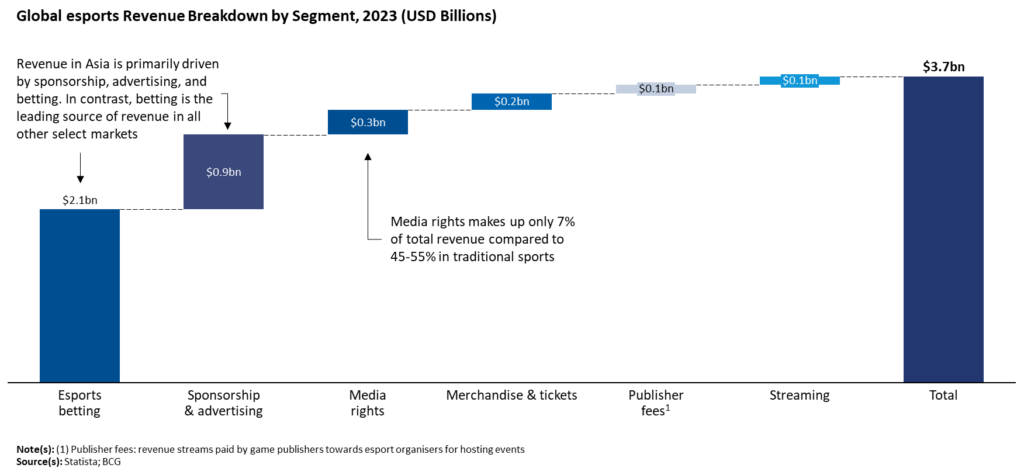

Betting drives the majority of revenue

The primary revenue sources for esports differ significantly from those of traditional sports. Unlike traditional sports, where media rights and sponsorships revenue streams dominate, esports receives nearly 60% of its global revenue from betting. Media rights account for 45-55% of revenue in traditional sports but represent only 7% in esports. This stark difference highlights the unique dynamics of the esports market and the growing influence of alternative revenue streams within the industry.

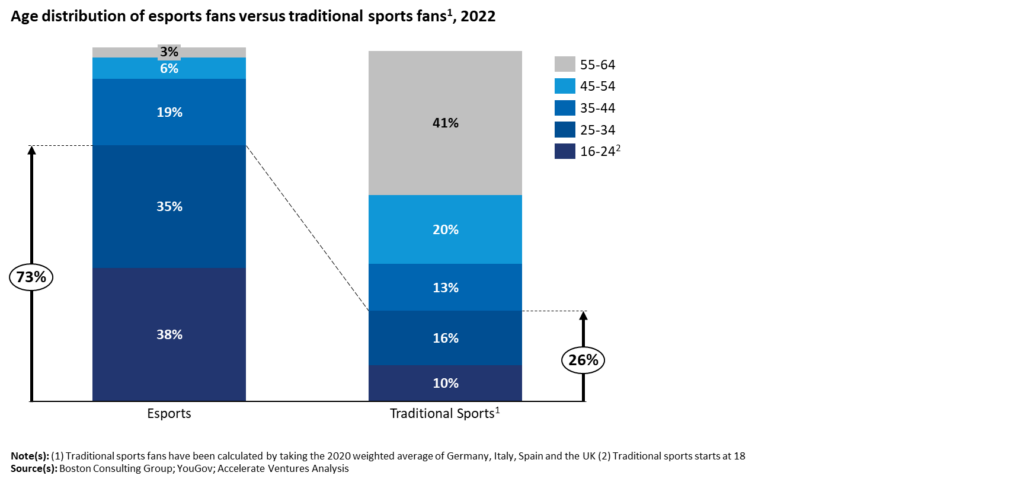

Driven by a predominantly young fanbase

Esports fans are notably younger than those of traditional sports, making them a unique and valuable audience. In 2022, the global esports fanbase surpassed 500 million, characterised by distinct demographics compared to traditional sports enthusiasts. Not only are esports fans younger, but they also tend to be more affluent and better educated – 30% of fans have an annual income exceeding $100,000. This demographic profile presents significant opportunities for brands seeking to engage a tech-savvy, high-earning audience.

The power of publishers

The structure of the esports market differs significantly from traditional sports, with publishers and game developers holding the most influence. These entities control the esports ecosystem by licensing their titles to league operators and deciding how much to invest in supporting competitive play. As a result, other stakeholders have limited power in shaping the landscape.

Publishers are often cautious about allowing esports participation, as poorly managed tournaments can lead to negative PR. Additionally, esports revenue remains a small fraction of overall gaming income – less than 1% of the total games market in 2022. For example, Nintendo only permits “Community Tournaments” under strict guidelines, reflecting the careful approach many publishers take.

The rise of mobile gaming

Mobile esports has gained significant traction in Asia and holds strong potential for continued growth. Mobile gaming offers a more affordable entry point into esports, making it accessible to a broader audience. This is particularly evident in the Asia-Pacific region, which is home to 80% of the world’s esports fans as of April 2023.

As mobile gaming continues to expand, it introduces new titles into a market traditionally dominated by only a few major PC games. This shift represents a promising growth area, as the rise of mobile esports diversifies the competitive landscape and draws in new participants.

Saudi Arabia’s prominent role

Saudi Arabia has rapidly emerged as a dominant player in the esports industry, with substantial investments coming primarily through its Public Investment Fund (PIF) and the PIF-owned Savvy Games Group (SGG). These investments span various aspects of the ecosystem, from tournament organisers to sponsorships and prize pools.

In 2022, SGG acquired the two largest esports organisers, ESL and FACEIT, for a combined $1.5 billion. This was followed by a $265 million investment in 2023 into the Chinese tournament organiser VSPO. Additionally, the PIF funds the Esports World Cup Federation, which not only oversees the Esports World Cup but also plans to offer annual grants to 30 top esports teams.

Saudi Arabia’s influence extends beyond organising events. SGG was the lead sponsor for both Gamers8 and the 2023 Global Esports Games, both of which took place in Riyadh. The country’s commitment to growing its esports footprint is further highlighted by the March 2024 launch of two dedicated gaming and esports venture funds worth a combined $120 million, led by Saudi Arabia’s National Development Fund (NDF). The PIF has also acquired significant stakes in major gaming companies, including Electronic Arts (9.2%), Take-Two Interactive (6.7%), Activision Blizzard (8.3%), and Nintendo (8.3%) as of March 2023.

Saudi Arabia’s investments have led to record-breaking prize pools in esports. The 2024 Esports World Cup in Riyadh will feature a $60 million prize pool, while Gamers8 2023 offered $45 million, setting a previous record. The Riyadh Masters 2024 also became the most lucrative Dota 2 tournament with a $5 million prize pool.

Esports has surged from a niche hobby to a global phenomenon, driven by rapid revenue growth and expanding market opportunities. With the US and Saudi Arabia emerging as major players, and mobile gaming introducing new dynamics, the industry is poised for continued evolution. As it matures, esports offers exciting prospects for innovation and investment worldwide.

![]()

Ready to take your sports start-up to the next level? Let's collaborate and redefine the game together.

What started as a $20,000 esports tournament in South Korea in 2000 has evolved into a global phenomenon, with the Esports World Cup in Riyadh now offering a staggering $60 million prize pool.

Over the past 24 years, esports has undergone explosive growth, driven by key milestones such as the rise of Twitch and the surge in streamers and viewers as a result of the Covid-19 pandemic. In just the last five years, esports revenue has more than tripled, reaching $3.8 billion in 2023. As a rapidly expanding industry, esports remains full of untapped revenue, presenting exciting opportunities in the years ahead.

Europe leads as the largest market

While Europe remains the largest market for esports globally, both now and in the foreseeable future, the US market is expanding at a much faster pace – growing three times quicker on average than Asia, Europe, and the UK. With a substantial population of gamers and esports enthusiasts, the US has seen esports rapidly gain traction as both entertainment and competitive sport. Notably, several US universities now offer esports scholarships and programs, further legitimising esports as a viable career path and attracting a new generation of players and fans.

Betting drives the majority of revenue

The primary revenue sources for esports differ significantly from those of traditional sports. Unlike traditional sports, where media rights and sponsorships revenue streams dominate, esports receives nearly 60% of its global revenue from betting. Media rights account for 45-55% of revenue in traditional sports but represent only 7% in esports. This stark difference highlights the unique dynamics of the esports market and the growing influence of alternative revenue streams within the industry.

Driven by a predominantly young fanbase

Esports fans are notably younger than those of traditional sports, making them a unique and valuable audience. In 2022, the global esports fanbase surpassed 500 million, characterised by distinct demographics compared to traditional sports enthusiasts. Not only are esports fans younger, but they also tend to be more affluent and better educated – 30% of fans have an annual income exceeding $100,000. This demographic profile presents significant opportunities for brands seeking to engage a tech-savvy, high-earning audience.

The power of publishers

The structure of the esports market differs significantly from traditional sports, with publishers and game developers holding the most influence. These entities control the esports ecosystem by licensing their titles to league operators and deciding how much to invest in supporting competitive play. As a result, other stakeholders have limited power in shaping the landscape.

Publishers are often cautious about allowing esports participation, as poorly managed tournaments can lead to negative PR. Additionally, esports revenue remains a small fraction of overall gaming income – less than 1% of the total games market in 2022. For example, Nintendo only permits “Community Tournaments” under strict guidelines, reflecting the careful approach many publishers take.

The rise of mobile gaming

Mobile esports has gained significant traction in Asia and holds strong potential for continued growth. Mobile gaming offers a more affordable entry point into esports, making it accessible to a broader audience. This is particularly evident in the Asia-Pacific region, which is home to 80% of the world’s esports fans as of April 2023.

As mobile gaming continues to expand, it introduces new titles into a market traditionally dominated by only a few major PC games. This shift represents a promising growth area, as the rise of mobile esports diversifies the competitive landscape and draws in new participants.

Saudi Arabia’s prominent role

Saudi Arabia has rapidly emerged as a dominant player in the esports industry, with substantial investments coming primarily through its Public Investment Fund (PIF) and the PIF-owned Savvy Games Group (SGG). These investments span various aspects of the ecosystem, from tournament organisers to sponsorships and prize pools.

In 2022, SGG acquired the two largest esports organisers, ESL and FACEIT, for a combined $1.5 billion. This was followed by a $265 million investment in 2023 into the Chinese tournament organiser VSPO. Additionally, the PIF funds the Esports World Cup Federation, which not only oversees the Esports World Cup but also plans to offer annual grants to 30 top esports teams.

Saudi Arabia’s influence extends beyond organising events. SGG was the lead sponsor for both Gamers8 and the 2023 Global Esports Games, both of which took place in Riyadh. The country’s commitment to growing its esports footprint is further highlighted by the March 2024 launch of two dedicated gaming and esports venture funds worth a combined $120 million, led by Saudi Arabia’s National Development Fund (NDF). The PIF has also acquired significant stakes in major gaming companies, including Electronic Arts (9.2%), Take-Two Interactive (6.7%), Activision Blizzard (8.3%), and Nintendo (8.3%) as of March 2023.

Saudi Arabia’s investments have led to record-breaking prize pools in esports. The 2024 Esports World Cup in Riyadh will feature a $60 million prize pool, while Gamers8 2023 offered $45 million, setting a previous record. The Riyadh Masters 2024 also became the most lucrative Dota 2 tournament with a $5 million prize pool.

Esports has surged from a niche hobby to a global phenomenon, driven by rapid revenue growth and expanding market opportunities. With the US and Saudi Arabia emerging as major players, and mobile gaming introducing new dynamics, the industry is poised for continued evolution. As it matures, esports offers exciting prospects for innovation and investment worldwide.

Accelerate Ventures 40-42 Hatton Garden London EC1N 8EB